Part II: Fingers in the Dam

In Part I, we traced the multi-millennial competition among monetary media — cowrie shells, glass beads, salt, silver, and finally gold — and argued that the progressive victory of more integral over less integral monetary forms was not a series of historical accidents but something closer to a natural law: as inevitable and impersonal as water finding its level. We also introduced a distinction that will carry increasing weight as the series develops: between hardness — the technical property of a high stock-to-flow ratio — and integrity, the fuller standard of which hardness is a necessary but not sufficient part. By the nineteenth century, the competitive process had produced the gold standard, a near-universal monetary anchor that imposed fiscal discipline on governments and provided a stable foundation for an era of remarkable capital formation and economic expansion. This installment examines how that anchor was cut, why the cutting was politically irresistible, and what the resulting drift has cost — and it traces, in some detail, the process of institutional centralization that made the cutting possible.

The Vulnerability That Hardness Could Not Cure

Gold’s emergence as the dominant monetary medium was, as Part I argued, the outcome of millennia of competitive selection. Its hardness was genuine: its supply could not be meaningfully expanded by human effort, its chemical properties made it indestructible across any human time horizon, and its global scarcity was a feature of cosmic chemistry rather than of any particular geography or technology. On the dimension of resistance to supply inflation, gold was without peer among naturally occurring substances.

But hardness, it turns out, is not the same as integrity. A monetary medium that achieves its discipline through physical scarcity retains one critical vulnerability: it exists in physical space, which means it can be located, accumulated, and seized. The history of the gold standard’s abolition is, at its root, the history of how this vulnerability was exploited — not in a single dramatic act, but through a decades-long process of institutional centralization that progressively concentrated gold into fewer and fewer locations, until the physical custody of the world’s monetary anchor resided in institutions that could be directed by political authority. When that concentration was complete, abolition required controlling not a dispersed private market but a handful of central banks and sovereign treasuries. The political will, when it came, found the preconditions already in place.

Understanding this centralization process is essential to understanding why the gold standard fell — and, as Parts V and VI will argue, to understanding what a genuinely integral money would have to look like in order to avoid the same fate.

The Long Centralization

The process was gradual, and at each stage it appeared not merely reasonable but necessary. The gold standard, to function at the scale of industrial national economies, required administrative infrastructure. Gold had to be assayed, stored, transported, and accounted for. The natural institutional home for that infrastructure was the central bank — an institution that, in most major economies, emerged or was formalized in the late nineteenth and early twentieth centuries precisely to manage the gold-based monetary system.

In the United States, the Federal Reserve Act of 1913 marked the decisive step. The Act created a centralized banking system with the authority to hold and manage the gold reserves that had previously been dispersed across thousands of national and state banks. The stated rationale was financial stability — to prevent the bank panics that had periodically convulsed the American economy, most recently in 1907. The effect, whatever the intention, was to concentrate monetary gold in twelve Federal Reserve Banks whose operations were ultimately coordinated by a single Board. The dispersal that had, however imperfectly, distributed the monetary base across a vast and varied private system was progressively replaced by a centralized structure whose governors were appointed by political authority.

The First World War accelerated the process dramatically. Within weeks of the outbreak of hostilities in August 1914, every major European belligerent suspended gold convertibility — because industrial-scale warfare required levels of government expenditure that simply could not be financed under a genuine gold constraint. Citizens were encouraged, and in some cases compelled, to surrender gold coins and jewelry to the war effort. Private gold flowed into sovereign custody on a vast scale. The monetary discipline was not merely suspended; the physical basis for restoring it was being systematically transferred from dispersed private hands into centralized state control.

After the war, the attempts to restore the gold standard were botched (more on that in Part IV) and ultimately abandoned. The wartime degradation of currencies against gold was simply too great to reconcile politically. An honest restoration would have required governments to re-peg their currencies to gold at their debased levels, transparently revealing the scale of wealth destruction wrought by wartime inflation — and by then the institutional infrastructure required for genuine restoration was no longer in place. What emerged in the 1920s was not the prewar gold standard but a series of managed approximations: the gold exchange standard, under which many nations held not gold itself but claims on the currencies of nations that did hold gold, primarily sterling and the dollar. The dispersal of genuine gold backing became thinner; the concentration of actual gold in a smaller number of institutions became denser.

The Great Depression provided both the ideological rationale and the political opportunity for the decisive act. On April 5, 1933, President Roosevelt signed Executive Order 6102, requiring all persons in the United States to deliver their gold coins, gold bullion, and gold certificates to the Federal Reserve at the official price of $20.67 per troy ounce. Violations were punishable by fines of up to $10,000 — around $250,000 in 2026 dollars — up to ten years in prison, or both, in addition to government seizure of the non-compliant gold. The confiscation was sweeping: within months, the overwhelming majority of privately held monetary gold in the United States had been surrendered.

That it was not total is worth noting — a minority of Americans held their gold through four decades of illegality, risking the full weight of the threatened penalties, all the way to re-legalization under President Ford in 1974. They were, in the precise sense the series has been developing, the Gresham’s Law actors operating at personal risk: those who understood what they held and refused to surrender it regardless of the legal cost. Their existence does not diminish the mechanism’s force — the centralization was functionally complete for political purposes. But their quiet defiance is a reminder that the coercive suppression of monetary gravity has never been without its dissenters. Every ounce that remained in private hands outside federal custody represented the mechanism continuing to operate beneath the surface of the law. The constitutional legality of EO 6102 was litigated all the way to the Supreme Court — which found in Perry v. United States (1935) that the abrogation of gold clauses was in technical terms unlawful, then held that no remedy existed. The constitutional framework designed to prevent exactly this kind of taking bent rather than held — a reminder that structural protections for property rights, however carefully designed, are ultimately only as durable as the political will to honor them under pressure.

The Gold Reserve Act of January 1934 then revalued gold from $20.67 to $35 per troy ounce — a 69% devaluation of the dollar against gold in a single administrative act. Citizens had been required to surrender their gold at the old price; the government immediately repriced it upward, capturing the revaluation gain for the sovereign and effectively confiscating roughly 40% of the real value of citizens’ monetary savings overnight. The sequence deserves to be stated with full clarity: first, the gold was centralized under the pretext of emergency; then, once centralization was complete and private recourse was impossible, the revaluation was executed. The order of operations was not accidental.

The Bretton Woods system, negotiated in 1944 as the institutional framework for the postwar monetary order, extended the centralization to the international level. Under Bretton Woods, the dollar was defined as convertible to gold — exclusively by sovereigns, not citizens — at $35 per troy ounce, and other major currencies were pegged to the dollar. In practice, this meant that the monetary gold of the Western world was overwhelmingly concentrated at a single location — Fort Knox — and the credibility of the entire international monetary system rested on the willingness of a single institution, the United States Treasury, to honor a single commitment. When that willingness faltered, the entire system could be terminated by closing a single window. That is precisely what Nixon did on the evening of August 15, 1971. The gold window was closed before markets could open on Monday. The announcement required no legislative process, no international negotiation, no gradual transition. It required one decision, by one authority, because the physical and institutional groundwork for that decision had been laid over the preceding six decades.

The lesson the centralization arc teaches is architectural: a monetary standard whose integrity depends on the physical custody of a material substance is a monetary standard with a structural vulnerability that no amount of political will or institutional design can permanently overcome. As long as the gold is somewhere, it can be taken — or its custodians can be instructed to withhold convertibility, which amounts to the same thing. The discipline the gold standard imposed was genuinely valuable. But it was provisionally valuable — contingent on the willingness of the custodians to honor the constraint — precisely because the material basis of the constraint was always available to be overridden by whoever controlled the custodial institutions. This is not a counsel against monetary discipline. It is an argument that genuine monetary integrity requires a form of discipline that is not contingent on the virtue or restraint of any custodian — because history’s consistent lesson is that the custodians, when sufficiently pressured, will not hold.

The Intellectual Architecture of Abandonment

The gold standard did not fail in any natural sense — it was not outcompeted by a more integral monetary medium, as every previous form of soft money had been outcompeted across the historical record. It was abolished precisely because of the discipline it imposed on the powerful. And what followed offers a revealing portrait of what the suppression of monetary gravity looks like in practice — and of the intellectual culture that enables it.

The 1914 War Loan was intended to raise £350 million for the British war effort. It raised less than a third of that from the public. Rather than disclose the failure, the Bank of England secretly plugged the shortfall through funds registered in the personal names of its Chief Cashier and his deputy, concealing the intervention on the Bank’s balance sheet under the anodyne heading of “Other Securities” rather than government debt. The Financial Times reported the loan oversubscribed, that applications were still pouring in, that the public had offered the government every penny it asked for and more. The cover-up remained hidden for over a century, until Bank of England researchers poring over aged ledgers published their findings in 2017 — at which point the Financial Times ran a follow-up noting that none of what it had originally reported was true.

What makes the episode particularly instructive is not merely the deception, but the reaction of the man who would later become the intellectual architect of the case against the gold standard. John Maynard Keynes, one of a handful of officials in the know, wrote a memo marked “Secret” in which he called the concealment “a masterly manipulation.” The man who would later indict the gold standard as a set of “golden fetters” constraining enlightened government began his career praising the covert monetization of government debt as a work of craft.

The sequence is worth remembering: the discipline was real, the temptation to circumvent it was irresistible, and the intellectual case for removing it permanently promptly followed. This is not to reduce Keynesian economics to its author’s early enthusiasm for a wartime deception — the economic arguments Keynes developed are serious and must be contended with in that spirit. But the biographical detail illuminates something important about the relationship between intellectual frameworks and the political environments that reward them. A theory that dignifies the removal of monetary constraints will always find more institutional support than one that insists on their necessity. The incentive to produce such theories is structural, not personal. And the history of post-gold monetary economics is, in considerable part, the history of that structural incentive being satisfied.

The System That Replaced It

What replaced the gold standard was something without precedent in the entire prior history of money: a global monetary system in which every major currency was a fiat currency — money created by government decree, backed by nothing but the legal obligation to accept it and the coercive power of the state to enforce that obligation.

This was not the market selecting a more integral monetary medium over a less integral one, as it had done reliably for millennia. It was the precise opposite: the state using legal coercion to suppress the natural gravitational process. When a government mandates that its paper currency be accepted as legal tender — and prohibits or penalizes the use of competing monetary media — it is not participating in monetary competition. It is ending monetary competition by force. And by ending it, it fools much of the population into acting in a manner that systematically prevents them from storing the energy represented by their labor in a form that preserves it.

The analogy to Gresham’s Law is exact, and it is deliberate. Gresham observed that bad money drives out good when both are given the same legal status. Legal tender laws enforce that equivalence by fiat. They do not change the underlying properties of the money — they simply prevent the market from expressing its preference for the more integral medium. The good money is still sought by anyone sophisticated enough to acquire it; the bad money circulates as required; and the mechanism of wealth transfer is reversed in direction but not in nature — flowing now from the population that holds the fiat currency to the sovereign that creates it, and from the uninformed citizen to the informed one.

This reverse pump is called seigniorage in its technical sense, but it manifests more broadly as inflation: the systematic erosion of the purchasing power of savings held in the fiat medium. The person who saves in dollars, pounds, or euros is doing exactly what the West African communities did when they saved in cowrie shells — saving in a medium whose supply is controlled by someone else, and that someone else has every incentive to expand to the holder’s detriment. The wealth transfer is less dramatic than a ship arriving with a hold full of shells, but it is structurally identical, and it is continuous and compounding.

The Compounding Pathologies

The deeper problem is that the suppression of monetary competition does not merely transfer wealth — it corrupts the entire system of price signals, capital allocation, and social trust on which a complex economy depends. And the mechanism through which it does so is, at its root, a single one: it raises the time preference of everyone operating within it.

Time preference is the degree to which a person — or a civilization — favors the present over the future. High time preference means consuming now, investing little, maintaining nothing, extracting what can be extracted before someone else does. Low time preference means deferring gratification, investing in the long term, building things meant to last, treating the future as real and worth sacrificing for in the present. It is not an innate psychological trait fixed by human nature. It is, to a significant degree, a rational response driven by self-preservation — and in the modern world that response is shaped above all by the monetary environment. When your savings lose purchasing power year over year, consuming now is rational. When your savings gain purchasing power year over year — when money held is money that will buy more tomorrow than it buys today — patience becomes the rational strategy. The monetary system does not merely reflect time preference; it sets it.

Integral money is therefore not merely a store of value. It is the civilizational infrastructure of low time preference — and low time preference is the civilizational infrastructure of everything else worth having: long-term planning and investment, durable buildings, careful stewardship of resources, the willingness to plant trees whose shade you will never sit under. Here again, we must be precise about what we are and are not claiming about the nineteenth century. The gold standard era was an era of comparatively long time horizons, because the monetary incentive pointed toward the future. When money holds its value over time, prices are meaningful across time: they can be compared year over year, decade over decade. Long-term investment becomes calculable. The interest rate reflects the actual time preferences of savers and borrowers rather than the preferences of a central committee. What it was not was an era of fully realized civilizational virtue — the long time horizons that characterized productive capital formation went hand-in-hand with child labor and the exploitation of colonial territories. The monetary lens illuminates the incentive structure. It does not determine how that incentive structure is used, or toward what ends. Those questions belong to a wider frame, one this series will reach in Part V.

Fiat money inverts the incentive structure. When the money supply can be expanded at will, prices no longer convey reliable information about scarcity. Interest rates manipulated by central banks send distorted signals about the true cost of capital, systematically encouraging borrowing and discouraging saving — which is to say, systematically encouraging present consumption at the expense of future productive capacity. The rational response to monetary inflation is to spend sooner rather than later, to borrow rather than save, to extract rather than steward. These may appear to be character flaws, but they are rational responses to the high time preference incentive landscape that fiat money creates. The pathologies that follow are the natural output of that landscape, applied across an entire civilization over multiple generations.

The migration of monetary premium. When money is soft, the monetary premium — the abstract store-of-value function that integral money would perform — does not disappear. It migrates. It leaks out of the currency and into whatever is harder: real estate, equities, art, commodities, any store of value that the market recognizes as more resistant to inflation. The prices of these assets are therefore no longer merely reflections of their intrinsic or utilitarian value. They carry an additional monetary premium inflated by the softness of the official currency. Housing becomes unaffordable not merely because of supply constraints or demographic pressure, but because it is serving a monetary function that integral money would have served itself. Stocks become inflated far beyond justifiable valuations, because savers are desperate to preserve their savings. This is not a conspiracy. It is hydraulics — the same hydraulics that governed every monetary competition in the prior historical record, now playing out within the borders of single nations rather than between civilizations.

The built environment and manufactured goods. The fiat-induced elevation of time preference does not confine itself to financial markets. It pervades the physical world of made things. A builder operating under an integral monetary system, in which future revenues are reliably calculable and the cost of capital reflects genuine time preferences, has every incentive to build durably: a building that lasts a century is worth the additional investment over one that requires replacement in thirty years. A manufacturer whose customers can save reliably and whose own cost structure is not distorted by artificially cheap credit has every incentive to make things that last, because durability is a competitive advantage in a world where consumers are not compelled to replace. Under fiat, these incentives reverse. Cheap credit and monetary inflation shorten every planning horizon. The return on durable construction is discounted against the certainty of near-term cost pressures. The result is visible everywhere: the architectural poverty of the built environment since the mid-twentieth century, in which ornament, craft, and structural permanence gave way to lightweight, synthetic, and inexpensive materials designed to be depreciated rather than inherited. But the monetary lens, applied here, reveals only the secondary cause. The pre-fiat built environment was not merely more durable — it was oriented. Its great buildings were built to disclose meaning, to anchor human beings within a sense of order larger than themselves, to express in stone and timber and glass a civilization’s orientation toward what is highest and most real. Their loss is the built environment expressing the same civilizational disorientation this series traces in every other domain — the collapse of a vertical, meaning-disclosing relationship with the world into a purely horizontal and instrumental one, now legible in every streetscape and suburb. What fiat money contributed was not the disorientation but its economic ratification: the systematic shortening of planning horizons, the cheapening of credit that made rapid construction and rapid depreciation rational, and the removal of the monetary pressure that would otherwise have rewarded permanence and craft as competitive advantages. Integral money would not automatically restore the orientation that gave the pre-fiat built environment its depth. But it would remove the specific economic conditions that have made every impulse toward permanence structurally irrational — and in doing so, it would reopen a space that the fiat system has systematically closed.

Fiat food. Nowhere is this dynamic more consequential, or more carefully obscured, than in the food supply. Industrial agriculture under the fiat system has been shaped by two converging forces: the inflation-driven pressure to reduce costs at the expense of quality, and the large-scale government subsidization of high-yield, chemically dependent monoculture farming — subsidies that are themselves a product of the fiat system’s removal of the constraint on government spending. The first of these forces would exist under any monetary system where competitive markets operate; what fiat money contributes is its systematic amplification, shortening planning horizons and inflating input costs in ways that make quality reduction not merely tempting but structurally rational.

The nutritional degradation of the food supply over the past half-century is not adequately captured by the official price indices, for a revealing reason. The basket of goods used to calculate the Consumer Price Index is periodically adjusted — ostensibly to reflect consumer behavior, but in practice to mask the true rate of monetary inflation. When a food item becomes too expensive for typical consumers, it is substituted in the index with a cheaper alternative; when product quality declines while the nominal price holds steady, the index records no inflation. This process of substitution and quality adjustment systematically understates the real erosion of purchasing power by treating the consumer’s forced migration toward lower-quality goods as a rational preference rather than a monetary consequence. The steak is replaced by ground beef in the index at the moment it becomes unaffordable, and the index records price stability. The ground beef is replaced by a processed meat product, and the index records price stability. The index is, in this sense, a measurement instrument calibrated to confirm the conclusion it is designed to support.

Meanwhile, the subsidization of industrial corn, soy, and wheat production — made possible by fiat-financed government intervention at a scale no hard-money fiscal constraint would permit — has reshaped the food system around inputs that are cheap to produce in large quantities rather than nutritionally optimal. The result is a food environment in which caloric density has increased while nutrient density has declined, in which processed food engineered from subsidized commodity crops has displaced whole food, and in which the chronic disease burden — obesity, type 2 diabetes, metabolic syndrome, cardiovascular disease — has expanded in near-perfect correlation with the entrenchment of the fiat-financed industrial food system. These are not coincidences. They are the downstream consequences of a monetary system that subsidizes the present at the expense of the future, applied to the domain most directly responsible for long-term human health.

Environmental extraction. The same logic applies, at the largest scale, to the natural world. Fiat money, by making monetary savings unreliable, creates a powerful structural incentive to extract value from whatever is real, scarce, and hard — the natural world foremost among them. When your currency loses purchasing power, you are incentivized to convert natural resources into financial claims faster than you otherwise would, because the resources themselves are a better store of value than the money. The fiat-induced elevation of time preference thus generates, mechanically and without anyone intending it, a systematic intensification of the extractive relationship with the natural world — an intensification operating independently of and on top of whatever extractive pressure the underlying technology and population growth would produce under any monetary system. The depletion of fisheries, forests, and mineral deposits under modern industrial capitalism is not simply a failure of environmental regulation. It is, among its several causes, deeply and systematically a monetary phenomenon — one whose contribution is distinct from and operates independently of the technological drivers of extraction capacity, and whose removal would alter the extractive calculus even where the technology remained unchanged.

War. No domain illustrates the compounding pathologies of fiat money more consequentially — or more invisibly — than war. The relationship runs deeper than pathology: fiat money is not merely an enabler of large-scale warfare but, in the modern era, its direct institutional product. As this essay has already traced, every major European belligerent suspended gold convertibility within weeks of August 1914, because industrial-scale warfare required expenditures that no honest monetary constraint could accommodate. The discipline had to be abolished before the killing could begin at scale. What emerged from that abolition then made the next war easier to finance, and the one after that easier still — a self-reinforcing loop in which war breaks the monetary constraint and the broken constraint removes the most powerful check on the decision to go to war. Integral money makes the cost of armed conflict immediately legible: it must be financed through taxation or honest borrowing, each of which presents the citizenry with a direct and visible bill at the moment the commitment is made. The discipline is not merely fiscal but democratic — it forces the question of whether the population is willing to pay for what its government proposes to do, before the doing rather than after. Fiat money dissolves this constraint entirely. The state can finance force projection through monetary expansion, distributing the cost as inflation across every holder of the currency, across years and decades, without any legible connection between the expenditure and the sacrifice it requires. Wars that would have been politically impossible to finance honestly become financially routine when the mechanism of payment is sufficiently diffuse and sufficiently deferred. The result is not merely that more and bigger wars are fought — it is that the decision to fight them is systematically insulated from the population that bears their cost: a transfer of democratic accountability as consequential as any transfer of wealth, and considerably less visible than either.

The debt-at-the-base inversion. Perhaps the most structurally peculiar pathology of the modern fiat system — and the one most consistently overlooked by both its defenders and its critics — is that it has placed debt itself at the foundation of the monetary order. Under the gold standard, the monetary base was a commodity: something real, scarce, and existing independently of any financial obligation. Under the modern fiat system, the monetary base consists primarily of government debt instruments. The dollar is, in a precise technical sense, a liability of the Federal Reserve collateralized by Treasury bonds, which are themselves obligations of the United States government. Money, in other words, is debt — and the entire monetary system rests on the perpetual expansion of that debt as its foundation.

This is worth pausing on in the context of the credit theory caveat entered in Part I. The credit theorists were right that money can originate in social promises and mutual obligations. What they cannot honestly claim is that this anthropological observation justifies the specific architecture of the modern fiat system — one in which the “promise” is made, not between parties with reciprocal social obligations, but by the most powerful institution in the system, against all holders of the currency, with no mechanism of accountability and no possibility of exit. Early credit money was a mutual compact enforced by community. Fiat debt money is a unilateral claim enforced by law. The superficial similarity — both involve “promises” — dissolves on inspection into a structural inversion. The former is a relationship between equals. The latter is a relationship between a sovereign with a monopoly on the ledger and citizens who have no alternative but to accept what the sovereign issues. Invoking the former to justify the latter is not theoretical sophistication. It is the confusion of a map with the territory it is supposed to represent.

This inversion produces an arrangement with the structural properties of a Ponzi scheme, not in the pejorative sense, but in the precise descriptive one: a system whose stability depends on continuous expansion. A Ponzi scheme does not collapse because of fraud — it collapses when the inflow of new participants can no longer service the obligations to existing ones. The debt-based monetary system has an analogous requirement: it requires perpetual growth in the monetary base — which means perpetual growth in debt — simply to service existing obligations and prevent deflationary collapse. This in turn requires perpetual growth in economic activity to generate the tax revenues and debt-service capacity that justify the expanding debt. Which in turn requires perpetual growth in population, in resource extraction, in productive throughput. The system cannot be in equilibrium. It must expand or it rapidly contracts toward crisis. Every recession is a moment at which the expansion briefly falters and the underlying structure becomes visible; every recovery is achieved by adding more debt to the base, expanding the system to a new and larger scale, at which the same fragility persists.

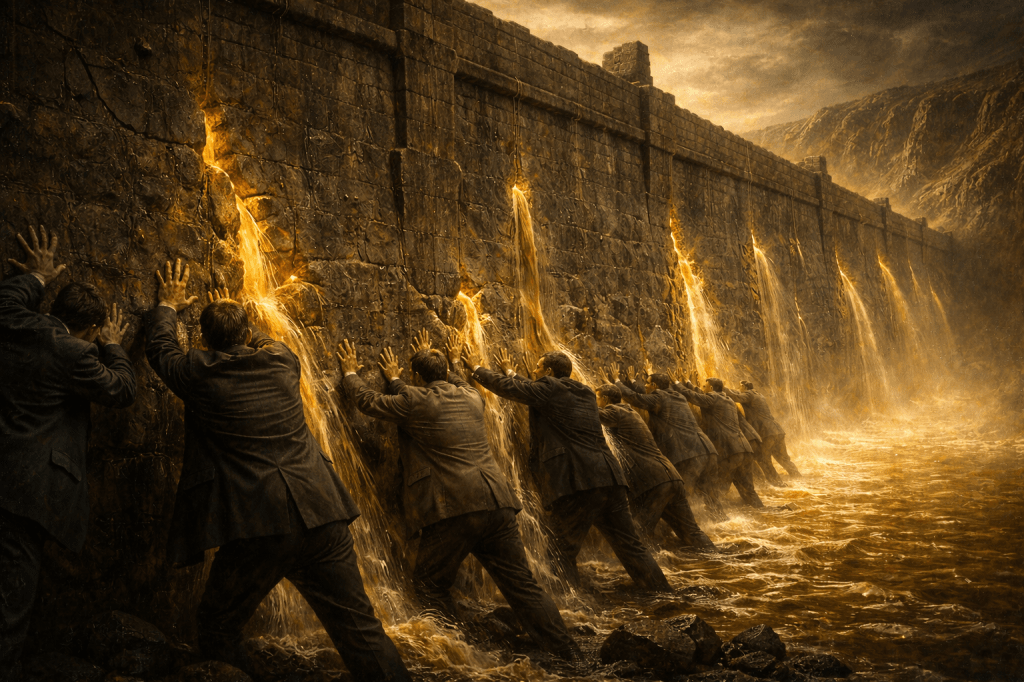

These are the predictable consequences of attempting, by state coercion, to suppress a natural law. Every intervention required to maintain the fiat system is evidence of pressure building behind the dam: the monetization of government debt, the suppression of interest rates toward or even below zero, financial repression (holding interest rates below the rate of inflation), the quantitative easing programs of the post-2008 era, the inflationary surges of the early 2020s. The fingers in the dam multiply because the cracks multiply.

What remains to be asked is who, politically, has an interest in keeping those fingers in place — and why the coalition turns out to be considerably stranger, and considerably more deeply entrenched, than it first appears. That is the subject of Part III.